Automotive Dealers Struggle to Recoup EV Investments

Automotive Dealers have spent heavily to get EV-ready, but uneven demand and shifting incentives are stretching payback timelines and patience.

I keep coming back to one simple truth about the EV transition: whatever the industry promises, the dealership has to make it real. Not in a keynote. Not in a concept sketch. In a service bay on a Tuesday, with a customer who wants honest answers, a sales team that needs confidence, and equipment that has to work every time.

That’s why this moment matters. Dealers have been asked to invest early—often heavily—so they can sell and support electric vehicles at scale. But the demand curve hasn’t behaved the way the spreadsheets expected. In some markets it’s strong and stable. In others it’s hesitant, incentive-driven, or constrained by charging reality and monthly payment math. When that happens, the dealer becomes the shock absorber for the entire system.

If you want a sense of how quickly the broader “car future” is shifting from hardware to systems thinking, we recently framed that transition through autonomy in Robotaxis in 2026: Are We Ready for Driverless Cities?. EV retail is the same story in a different outfit: the technology matters, but the supporting system matters more.

Why does this matter right now?

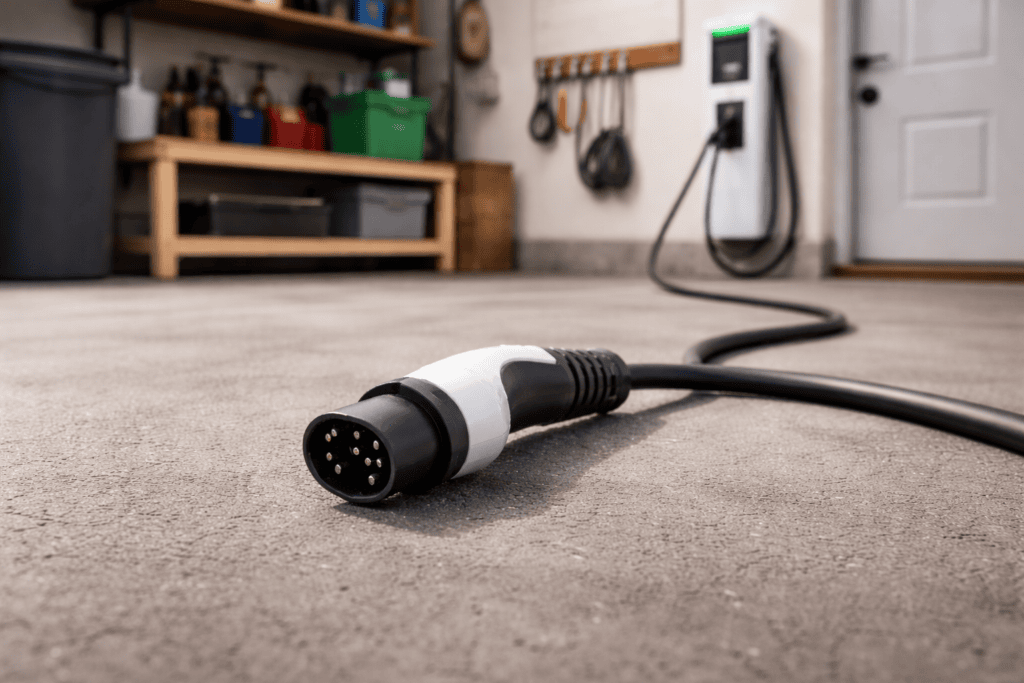

Because the EV transition has moved from “strategic direction” to “operational bill.” The costs are no longer theoretical. They’re tangible line items: chargers, electrical service upgrades, high-voltage tools, technician training, safety procedures, and sometimes facility redesigns to accommodate a different kind of workflow.

Industry estimates have made the scale of the investment hard to ignore. The National Automobile Dealers Association has said franchised dealerships anticipate investing billions to build out EV retail readiness, including charging infrastructure and facility upgrades. You can see the organization’s broader data and reporting hub directly at NADA Data.

That investment is landing at the same time the U.S. EV market is proving it can be volatile quarter to quarter. Cox Automotive’s Kelley Blue Book tracking showed EV share peaking in Q3 2025 and then dropping sharply in Q4, a swing that matters because it changes how long cars sit, how much incentive pressure builds, and how confident dealers feel about ordering and stocking. The most direct snapshot is the Cox Automotive Q4 2025 EV sales commentary.

When EVs sit longer, costs don’t just rise on the vehicle side. The investment made to support EV sales and service can’t be “unmade” just because demand softened. A charger doesn’t get cheaper because it’s underused. A trained technician doesn’t become free because EV appointments are sporadic.

And the pressure isn’t only on sales. As we talked about in The New S-Class Is Mercedes’ Answer to Tesla’s Hype, the modern auto story increasingly lives in software, confidence, and customer workload reduction. Dealerships are being asked to deliver that same confidence for EVs—often before the category is predictable enough to reward it consistently.

Trade reporting has been blunt about the near-term mismatch: incentives have shifted, costs remain high, and dealers are trying to earn back charging and training spend while the market recalibrates. A clear example is this analysis from WardsAuto: EV incentives dry up, costs stay high.

How does it compare to rivals or alternatives?

The fairest comparison is not “EVs versus gas” in the abstract. It’s EVs versus the alternatives that lower fuel use and emissions with less behavioral change: hybrids and plug-in hybrids.

For many shoppers, hybrids are the low-drama choice. They reduce fuel use without requiring home charging, and they fit existing routines. From a dealer perspective, they also fit existing retail operations more cleanly: familiar sales conversations, predictable service patterns, and fewer infrastructure dependencies.

Plug-in hybrids split the difference. In the best-case scenario, they handle daily miles electrically and keep gasoline for road trips. In the worst-case scenario, they behave like regular hybrids because owners don’t charge them. Even that “worst case” is easier for many consumers to accept than the full leap to a battery-electric vehicle in areas where public charging is inconsistent or where renters can’t easily install home charging.

That’s the key competitive reality: a buyer isn’t just choosing a car; they’re choosing a system. If the system feels risky—range uncertainty, charging reliability, resale value swings—many shoppers pick the alternative that delivers most of the benefit with less perceived downside.

We’ve seen the same consumer logic play out in other categories where “aspiration” collides with “practicality.” Our piece on Mattel Brick Shop Redefines Dream Car Ownership made a similar point in a different lane: enthusiasm adapts when the real-world version of ownership becomes harder to justify.

For automakers, that pressure is pushing product planning back toward flexibility: more hybrids, more mixed powertrain strategies, and more focus on affordability. Reuters captured that strategic reset succinctly in Carmakers’ answer to US EV lull: hybrids, cheaper models.

Who is this for and who should skip it?

This matters if you’re an EV-curious buyer, an EV owner, a dealer operator, an automaker, or anyone trying to understand why the EV transition can feel inconsistent across regions.

If you’re shopping, this explains why the experience can vary dramatically from store to store. Some dealers are fluent and confident. Others are cautious because the economics haven’t worked cleanly in their market yet. That doesn’t automatically mean the technology is flawed. It often means the payback timeline is unclear.

If you already own an EV, dealer readiness affects your service reality. A stronger local dealer network makes ownership easier, especially when you need help quickly.

If you work in auto retail, this is simply naming the pressure: the industry is asking dealers to finance a transition while the demand signal remains noisy.

Who should skip it? If you only want the EV story as a culture-war argument—either triumphalist or dismissive—you’ll miss the practical truth. This is an economics and operations story more than an ideology story.

What is the long-term significance?

This tension will shape what the dealership becomes over the next decade.

First, it accelerates consolidation. EV readiness is easier for large dealer groups that can spread investment across multiple rooftops, negotiate utility upgrades at scale, and run centralized training programs. Smaller stores can do it, but the risk is sharper when permitting delays or unexpected electrical work hits a single location’s budget.

Second, it forces a rethink of the service business. EVs do change routine maintenance patterns, but they also introduce new service needs: software diagnostics, battery health evaluation, thermal management, high-voltage component repair, and a different kind of warranty work that requires training and process discipline. Dealers that build those capabilities early can become trusted local centers for a new kind of ownership relationship.

Third, it raises the stakes for used EV retail. The used market is a key adoption bridge because it lowers the price of entry, but it requires clear standards for battery condition and a straightforward way to explain real-world range and charging habits. Dealers who can certify and explain used EVs responsibly will earn trust; those who can’t will watch shoppers migrate to simpler-feeling marketplaces.

Finally, it pressures automakers to treat dealers less like a distribution channel and more like a co-investor. When a franchise partner spends real money, they expect predictability: product cadence, incentive strategy, clear communication, and service support that doesn’t feel improvised.

The quiet takeaway is that a slower adoption curve isn’t the end of EVs. It’s a reminder that “the future” still has to clear a monthly payment, a charging plan, and a service appointment. Dealers are trying to build that future in real time. The rest of the industry should take seriously what it costs them to do it.